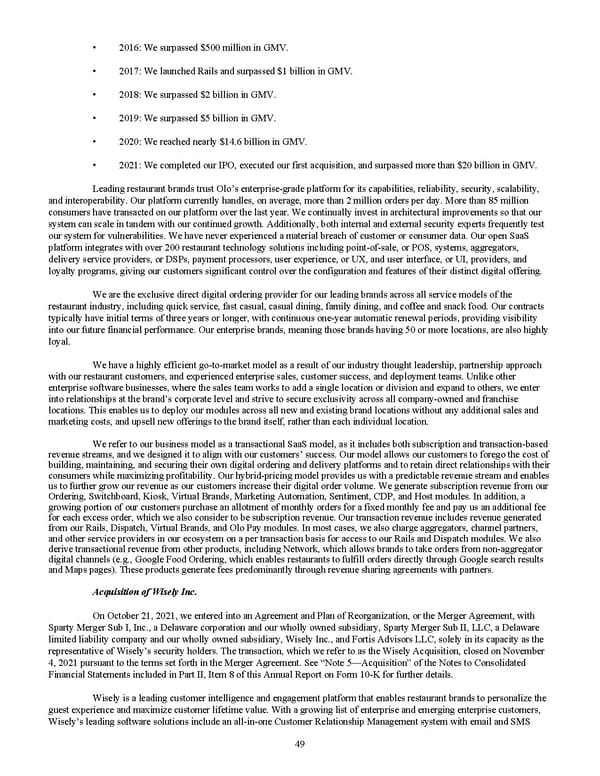

• 2016: We surpassed $500 million in GMV. • 2017: We launched Rails and surpassed $1 billion in GMV. • 2018: We surpassed $2 billion in GMV. • 2019: We surpassed $5 billion in GMV. • 2020: We reached nearly $14.6 billion in GMV. • 2021: We completed our IPO, executed our first acquisition, and surpassed more than $20 billion in GMV. Leading restaurant brands trust Olo’s enterprise-grade platform for its capabilities, reliability, security, scalability, and interoperability. Our platform currently handles, on average, more than 2 million orders per day. More than 85 million consumers have transacted on our platform over the last year. We continually invest in architectural improvements so that our system can scale in tandem with our continued growth. Additionally, both internal and external security experts frequently test our system for vulnerabilities. We have never experienced a material breach of customer or consumer data. Our open SaaS platform integrates with over 200 restaurant technology solutions including point-of-sale, or POS, systems, aggregators, delivery service providers, or DSPs, payment processors, user experience, or UX, and user interface, or UI, providers, and loyalty programs, giving our customers significant control over the configuration and features of their distinct digital offering. We are the exclusive direct digital ordering provider for our leading brands across all service models of the restaurant industry, including quick service, fast casual, casual dining, family dining, and coffee and snack food. Our contracts typically have initial terms of three years or longer, with continuous one-year automatic renewal periods, providing visibility into our future financial performance. Our enterprise brands, meaning those brands having 50 or more locations, are also highly loyal. We have a highly efficient go-to-market model as a result of our industry thought leadership, partnership approach with our restaurant customers, and experienced enterprise sales, customer success, and deployment teams. Unlike other enterprise software businesses, where the sales team works to add a single location or division and expand to others, we enter into relationships at the brand’s corporate level and strive to secure exclusivity across all company-owned and franchise locations. This enables us to deploy our modules across all new and existing brand locations without any additional sales and marketing costs, and upsell new offerings to the brand itself, rather than each individual location. We refer to our business model as a transactional SaaS model, as it includes both subscription and transaction-based revenue streams, and we designed it to align with our customers’ success. Our model allows our customers to forego the cost of building, maintaining, and securing their own digital ordering and delivery platforms and to retain direct relationships with their consumers while maximizing profitability. Our hybrid-pricing model provides us with a predictable revenue stream and enables us to further grow our revenue as our customers increase their digital order volume. We generate subscription revenue from our Ordering, Switchboard, Kiosk, Virtual Brands, Marketing Automation, Sentiment, CDP, and Host modules. In addition, a growing portion of our customers purchase an allotment of monthly orders for a fixed monthly fee and pay us an additional fee for each excess order, which we also consider to be subscription revenue. Our transaction revenue includes revenue generated from our Rails, Dispatch, Virtual Brands, and Olo Pay modules. In most cases, we also charge aggregators, channel partners, and other service providers in our ecosystem on a per transaction basis for access to our Rails and Dispatch modules. We also derive transactional revenue from other products, including Network, which allows brands to take orders from non-aggregator digital channels (e.g., Google Food Ordering, which enables restaurants to fulfill orders directly through Google search results and Maps pages). These products generate fees predominantly through revenue sharing agreements with partners. Acquisition of Wisely Inc. On October 21, 2021, we entered into an Agreement and Plan of Reorganization, or the Merger Agreement, with Sparty Merger Sub I, Inc., a Delaware corporation and our wholly owned subsidiary, Sparty Merger Sub II, LLC, a Delaware limited liability company and our wholly owned subsidiary, Wisely Inc. , and Fortis Advisors LLC, solely in its capacity as the representative of Wisely’s security holders. The transaction, which we refer to as the Wisely Acquisition, closed on November 4, 2021 pursuant to the terms set forth in the Merger Agreement. See “Note 5—Acquisition” of the Notes to Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K for further details. Wisely is a leading customer intelligence and engagement platform that enables restaurant brands to personalize the guest experience and maximize customer lifetime value. With a growing list of enterprise and emerging enterprise customers, Wisely’s leading software solutions include an all-in-one Customer Relationship Management system with email and SMS 49

2022 10K Page 55 Page 57

2022 10K Page 55 Page 57